Another Mega-Oil Deal

That’s two mega oil deals in a span of about three weeks.

On October 11, Exxon-Mobil (NYSE: XOM) announced it would acquire Pioneer Natural Resources (NYSE: PXD) for $60 billion. Pioneer has the rights to 850,000 acres in the Permian Basin. Add that to 570,000 acres in the Permian Basin Exxon already has, and Exxon is now the dominant player in the Permian.

Plus, to quote the New York Times:

Exxon has spent decades investing in projects around the world, but the deal would squarely lodge its future close to its Houston base, with most of its oil production in Texas and along the coast of Guyana.

Exxon has its Eagle Pass LNG terminal coming online for global export next year. The terminal sits on the Texas-Louisiana border, so having feedstock as close as the Permian Basin in Western Texas is an obvious benefit.

Now, today, Chevron (NYSE: CVX) says it is acquiring Hess (NYSE: HESS) for $53 billion. The deal will add about 10% to Chevron’s daily production. And, to quote the Times again:

Hess has a strong position in Guyana, where major oil discoveries have been made in recent years and where Chevron’s rival, Exxon, is the key operator. Hess is also a leader in the Bakken shale area of North Dakota.

Guyana again…

Guyana and neighboring Suriname are home to the biggest oil discovery of the last 15 years at least. The shallow water Guyana-Suriname basin may hold as much as 30 billion barrels of recoverable oil. And it is the light sweet variety, with production costs estimated to be as low as $28 a barrel.

Exxon and Hess were the biggest players in the Guyana-Suriname Basin. Obviously, now that Hess is being acquired, Chevron becomes a major player.

But there’s another smaller player that could be sitting on as much as 10 billion barrels in the Guyana-Suriname Basin. The stock has rallied 15% since Exxon acquired Pioneer. And now that Chevron is moving into the Guyana-Suriname Basin, this stock is clearly an buyout candidate…

This oil stock is currently valued at just under $1 billion. It trades just below $11 and has a forward P/E of 4. Any buyout would likely come with at least a 50% premium to the current share price, maybe more.

Back in September, I included this stock in a Special Report for Pro Trader Today readers called Top 8 Oil Stocks to Own Now. It’s totally free, check it out right here.

Demand Outlook for Oil

When acquisition activity heats up for oil, it’s reasonable to wonder if the majors like Exxon and Chevron are expecting to see a spike for oil demand and oil prices. And by extension, it’s reasonable to wonder if so-called Peak Oil – the point at which demand for oil peaks and starts to fall – may be more elusive than some industry experts have estimated.

It’s an especially relevant question considering that there’s some concern about the real strength of EV demand – enough to wonder if EVs are really capable of sapping demand for oil.

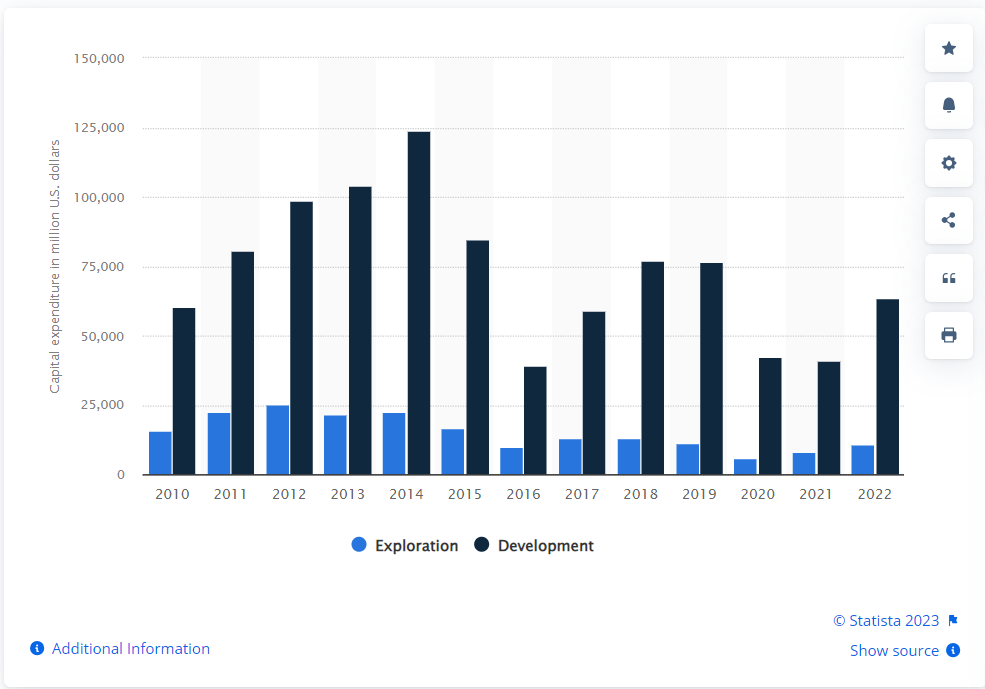

Here’s a nice chart to start the discussion:

This chart from Statista is titled: Capital expenditure on exploration and development by the United States oil and gas industry from 2010 to 2022

It shows that U.S. oil companies are spending a bit less on exploration and a lot less on development. And this fits nicely with the outlook for oil demand.

The International Energy Agency estimates that global oil demand will increase to ~105 million barrels a day in 2028, at which point demand growth effectively stagnates.

The IEA goes on to say that strength in petrochemicals and aviation fuels offsetting declines in transportation fuels (gasoline and diesel, which make up around 70% of all oil demand) is what will keep demand essentially stable.

So the common assumption that increased adoption of electric vehicles (EVs) will lead to a decrease in gasoline demand can exist right alongside the assumption that the world is still at least 5 years away from Peak Oil.

And if you look at it from the oil companies point of view – you gotta ask “what do they care if it’s gasoline or petrochemicals and aviation fuels? So long as oil demand stays at 100 million barrels a day or higher for the next decade, they can do just fine.”

What’s more, looking at that chart again, what incentive do oil companies have to increase their spending on exploration and development? To put that another way, if supply and demand are roughly in balance, and demand is not expected to grow significantly, why would you spend money to increase supply?

We saw what oversupply can do back in 2014-15, when oil prices crashed from $100 to $35 a barrel. Rest assured U.S. oil companies don’t want to go through that again.

The best strategy for oil companies in general is to manage their costs for a static market. And that means it makes more sense for a company like Exxon to add to its own output via an acquisition than it does to spend money on exploration that would serve to increase overall supply and potentially drive prices lower.

And especially in Exxon’s case, buying more Permian Basin production that is close to its own infrastructure (Eagle Pass LNG terminal) likely comes with cost benefits – a savvy move.

Forget Drill Baby, Drill

Another Mega-Oil Deal

The notion that if the U.S. would just remove any restrictions on drilling, open up the Florida coast and the Alaskan wilderness to oil exploration and development would lead to a mad scramble by oil companies to increase production ~13 million barrels to the point that the U.S. is truly energy independent – around 25 million barrels a day – is just silly.

Prices would collapse.

If you want to invest in oil stocks, there are two ways to go. One: focus on the majors that have the best ability to manage costs and increase their dividend. It’s a short list, headed by Exxon-Mobil. And two: focus on smaller companies that could become acquisition targets. With Hess and Pioneer just gobbled up, that list just got smaller.

That’s what I got for you today, take care and I’ll talk to you on Wednesday…

Briton Ryle

Chief Investment Strategist

Pro Trader Today

brit.ryle@protradertoday.com

Facebook: https://www.facebook.com/ProTraderToday

Twitter: https://twitter.com/BritonRyle