CPI: To Core, or Not To Core

Despite all the recent commentary from the various Fed governors that they stand ready to do more to combat inflation, this morning’s CPI number confirms what the market already knows: the Fed is done hiking interest rates.

The CPI rose at a 3.2% annualized rate in October. And remember, that inflation number comes right on the heels of a massive surge for GDP growth (4.9%) in the third quarter. If there was ever going to be a resurgence for inflation, it seems reasonable that it would happen right along with a big surge in growth…

But if you’ve been paying attention, despite a quick spike for oil after the Hamas attack on Israel, oil prices have been trending lower mid-September. And that has clearly weighed on inflation.

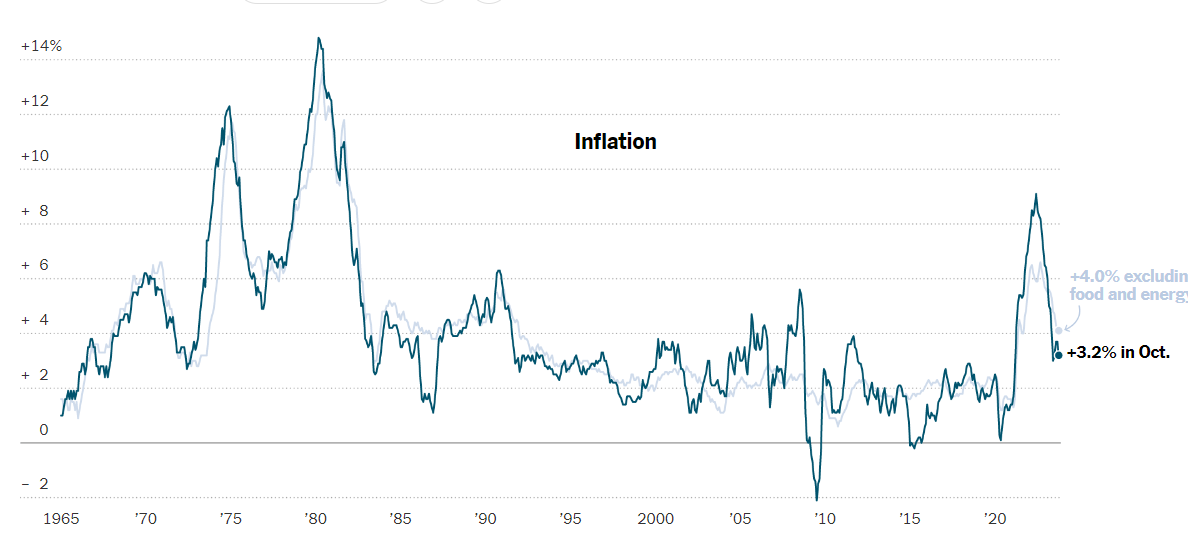

Bigger picture: the decline for CPI has been pretty stunning all year. Here’s a chart from the New York Times that shows the trend clearly:

Now, there’s a funny thing with how the Consumer Price Index (CPI) is reported. There’s the regular CPI, which tracks a wide range of prices for food, energy, rent, new and used cars, etc. Then there’s the so-called “core” CPI which ignores food and energy prices.

There are a fair amount of people that don’t like the core, exactly because it ignores food and energy prices. After all, food and energy are significant expenses for any household. So the logic goes that if you ignore big expenses like food and energy, well, you’re ignoring the real day-to-day impact of inflation…

I tend to counter that logic with 2 observations. One, while oil prices themselves can be inflationary, in that higher transportation costs get passed onto the consumer – oil prices are not necessarily high because of inflation. For instance, whatever strength we’ve seen for oil prices in the last 6 months have come because Saudi Arabia and Russia got together and cut daily production by 2 million barrels a day, for the overt purpose of pushing oil prices higher.

As I’ve said in the past, if the Fed considers oil prices as part of its decision to hike rates and slow the economy, the Fed is in effect letting Saudi Arabia and Russia influence U.S. monetary policy. Seems like a bad plan…

Second, the majority of the price increases for food we’ve seen this year are the result of what I call Artificial Inflation (AI). Food companies have taken full advantage of the cover of an inflationary environment to hike prices far beyond the degree to which their own costs have risen.

I’ve written about Artificial Inflation here and here, and it absolutely qualifies as price gouging. And of course, no politician will call the food companies out on this because…SuperPac. So it’s reasonable that the Fed should turn a blind eye to Artificial Inflation, and not let food prices influence rate hikes that ultimately just puts workers out of their jobs…

A Little Consistency, Please

I bring all this up because the various talking heads will jump back and forth between the regular CPI – the so-called “headline” number – and the core CPI number as it suits their purpose (which is usually to push the “inflation is declining” narrative)…

So back in the summer, when oil prices were rallying, the talk was always about the core CPI number, that ignores energy and food.

But THIS time around, it’s the headline number that’s getting the, um, headlines. Because THIS time around, oil prices actually fit the “inflation is declining” narrative.

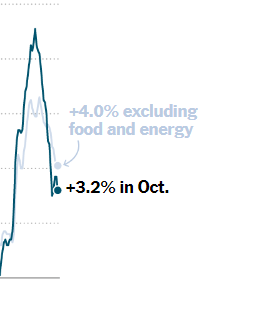

And it’s really hard to see on the chart above, but the core CPI number is a lot stronger for October. Here’s an enlargement of the relevant part of that chart…

The Times very sneakily put a little shadow chart to show the core CPI number behind the bold chart that shows the headline number.

All this isn’t to say that a lower headline CPI number isn’t good. It is. But why not make the best of it, ignore the stronger core number, and add on to what’s already been a rip-snorting rally?

Still, seems to me a little consistency in how economic data is reported might be nice.

Oh, Fisker

I’ve been pretty adamant that there are only two pure EV makers worthy of investors attention: Rivian (NASDAQ: RIVN) and Fisker (NASDAQ: FSR). Sadly, recent news from Fisker may whittle my list down to one.

I’m not sure it’s worth getting into all the details, but Fisker shares are getting crushed by the double whammy of an apparent slowing of demand for EV and its own internal execution problems.

I’m removing Fisker from the Pro Trader Today Recommended Buy list, but I’m leaving Rivian on it.

Rivian is still delivering vans to Amazon, that’s a pretty solid source of demand. I’m not really surprised that there are ebbs and flows to consumer demand for EVs. And the price cuts that we are seeing should stoke demand at some point. But I suspect there weil plenty of notice if/when demand does start to rebound. So consider the whole sector a “hold” right now.

That’s it for me today, take care and I’ll talk to you on Wednesday…

Briton Ryle

Chief Investment Strategist

Pro Trader Today

brit.ryle@protradertoday.com

Facebook: https://www.facebook.com/ProTraderToday

Twitter: https://twitter.com/BritonRyle