Oil Prices and Recession

You can’t really say it’s happened all of a sudden. For the last year, economists and market strategist-types have been talking about an imminent recession for the U.S. economy. Inflation, interest rates, the war in Ukraine, commercial real estate, the mini-bank crisis back in March, overheated labor market – the list of imminent catalysts is very long.

To this point, none of them have managed to put more than a little dent in the U.S. economy. Frankly, the resilience of the U.S. economy has been impressive – enough so that a fair number of recessionistas have abandoned their bearish calls.

Bank of America just recently raised its year end forecast for the S&P 500 to 4,600. Analysts have been raising their estimates for third quarter earnings season, which starts on October 15…

Savita Subramaniam is Bank of America’s head of U.S. Equity and Quant Strategy at BofA just put out a note that said:

“I see far more bullish indicators for mid and large-cap stocks than I do bearish…What I find interesting is that every day a new bearish narrative emerges.”

And she’s right – seems like every single day some new end of the world story hits the wire and pushes stock prices lower.

Over the weekend, Bloomberg put on a full-court press about imminent recession.

Now, it’s important to understand that while economists will point to any number of catalysts, the real cause of a recession is a decline in consumer spending.

The U.S. economy is +70% driven by consumer spending, and so in order to get the consecutive quarters of negative GDP growth necessary to call a recession, consumers have to cut spending.

Bloomberg attempts to point out several things that could cause consumers to spend less: higher oil prices, the resumption of student loan payments, autoworkers strikes – and even the end of Taylor Swift’s record-breaking tour!

Yeah ok, I guess Swifties aren’t spending on tickets and getting hotel rooms anymore. At least not until next year, when she’s back on the circuit. But c’mon, is this recessionary?

I’ve read that, in total, Taylor Swift and Beyonce concerts added $8.5 billion to third quarter GDP. Pretty amazing. But you know, US GDP will end 2023 around $26 trillion dollars. $8.5 billion less because Swift and Beyonce are chilling at home for a few months (or in Travis Kelce’s box seats at Arrowhead), that’s what you call a “blip.”

Sadly, this is not the kind of detailed analysis I’ve come to expect from Bloomberg…

And neither is the contention that people talking about a “soft-landing” raises the odds that there won’t be a soft-landing. The article asks:

“Why do economists find it so difficult to anticipate recessions? One reason is simply the way forecasting works. It typically assumes that what happens next in the economy will be some kind of extension of what’s already happened — a linear process, in the jargon. But recessions are non-linear events. The human mind isn’t good at thinking about them.”

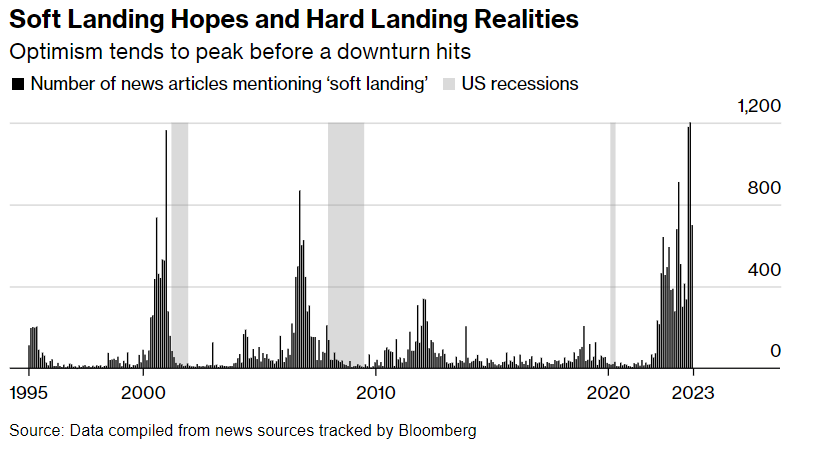

And offer this chart as evidence:

The gray areas are recessions, positioned as the inevitable outcome of news articles predicting a soft-landing. (As an aside: I was around for the 2000 and 2008-9 recessions, I don’t recall the term “soft-landing” being used at all. I would’ve guessed this was a relatively new phrase, which is why the chart shows such heavier use of the term “soft landing” in 2023.)

This chart purports to show 3 instances of recession being immediately preceded by discussion of a soft-landing. But really, only two examples over the last 25 years are worth mentioning. Because the last example was the recession caused by COVID, and that was utterly unrelated to anything that was happening in the economy. In fact, economic data had been improving in late 2019, before COVID hit.

Now, the point made in the quote I included – that recessions are non-linear events – is 100% correct. It is sudden shocks to the system that cause consumers to dramatically slow their spending. So Bloomberg suggesting that the inability to forecast a surprise recessionary shock to the economy – which is always the case – is somehow evidence that recession is imminent is really a stretch.

Now, if you want to argue that higher oil prices, an autoworker strike and the resumption of student loan payments makes the economy more vulnerable to a shock, that those factors would exacerbate some Black Swan event, sure, that’s valid.

But it doesn’t – in any way – mean that a shock is imminent. Sudden shocks are ever-present. A massive terrorist attack, an outbreak of war, a pandemic – these things can strike at any time. Investing or trading decisions based on whatever Black Swan event could happen is not a very good plan.

If you ask me, Bloomberg is fear-mongering – if you don’t think the Big Money hedge funds use the financial media outlets to try and push stock prices around, well…

Oil Prices

Now you probably know that inflation has ticked up recently, largely because oil prices have surged over the last couple of months.

I’ve heard a few calls for the Fed to resume its rate hike campaign to fight this new aspect of inflation.

Of course it’s true that higher oil prices will send prices higher. If it costs more to ship stuff, you can bet those added costs will show in the price of stuff. But I’m not so sure that these price hikes should be thought of as inflation. At least not in the traditional sense. Because the reason oil prices have surged higher doesn’t have anything to do with the strength of the U.S. economy…

Yes, oil demand has improved this year. And U.S. production has improved too – hitting a record 13 million barrels a day. But that doesn’t offset the 2 million barrels a day that Russia and Saudi Arabia have taken off the market – and are promising to keep off the market through the end of this year.

The Fed probably could choke off some demand and get lower prices for oil by hiking interest rates further. Higher interest rates will also raise the risk of recession. Because while we know the labor market has remained strong so far, there is a limit. Keep hiking rates and at some point, the labor market will crack. Get enough people fired from their jobs, to the point where the unemployment rate jumps, that’s a pretty good way to get consumer spending to fall and bring on that recession.

But the thing is: if the Fed hikes to combat oil induced inflation that is a direct result of Russian and Saudi production cuts – aren’t we letting Putin and MBS call the shots on U.S monetary policy?

Seems like a bad plan…

Seems to me nothing would make Putin happier than to see the U.S. fall into recession. If people are losing their jobs, you can bet there’ll be a lot more opposition to U.S. support for Ukraine.

Briton Ryle

Chief Investment Strategist

Pro Trader Today

brit.ryle@protradertoday.com

Facebook: https://www.facebook.com/ProTraderToday

Twitter: https://twitter.com/BritonRyle

P.S. Make sure you download my new report Top 8 Oil Stocks To Own Now… It’s totally FREE!

Array