Drill, Baby, Drill is Dead

I’ve had this article in the hopper for a couple weeks. I started it after I watched the last GOP presidential debate back on November 8. I was fired up because every single one of the candidates offered up the exact same line about America’s energy situation.

Basically, some version of “drill, baby, drill.”

Whether it was how to combat inflation, how to extricate ourselves from abusive relationships with middle eastern countries or Venezuela, or even how to ensure that Social Security continues — every single one of the candidates offered up the same conclusion: high oil and gasoline prices are the source of all of America’s ills.

So, if we just complete the Keystone Pipeline, approve any and all drilling applications, drop EPA regulations — American oil companies will all fall in line, boost production to the point that America is truly energy independent and push oil prices down to $50 a barrel, break the back of inflation and save social security.

In other words: drill baby, drill. It’s a pervasive belief these days. It’s also wrong…

ECON 101

Ask Exxon-Mobil (NYSE: XOM) how it feels about oil prices…

Would Exxon want to spend billions of dollars to boost production and crush oil prices? Seems unlikely…

And just as important: do any of Exxon’s investors want to see the oil giant spend money to raise production and lower prices so that the company can make less money?

It’s been my experience that investors tend to prefer investing in companies that grow revenue and manage costs to boost earnings.

Now obviously, the function of supply and demand is about the most basic economic formula. It’s Econ 101.

When demand for a thing is higher than supply, that thing’s price will rise. And typically, when the price for a thing is high, companies capable of providing that thing will increase production to take advantage of strong pricing. And so it is virtually inevitable that supply will eventually overwhelm demand, prices will fall and CAPEX investment will be lost.

And the interplay between supply and demand couldn’t be any easier to see than it is in the oil market.

A Brief History of the Modern Oil Market

2005 was the year where oil prices first crossed the $50 a barrel mark.

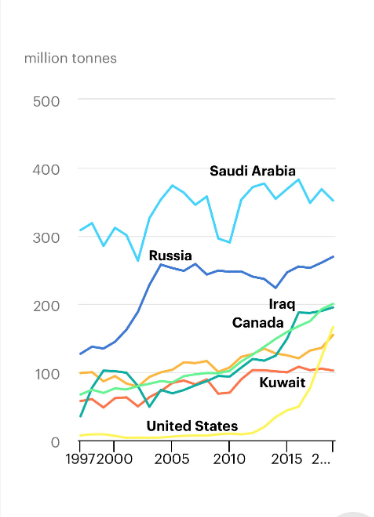

Oil supply was dominated by OPEC, Russia, Mexico and Canada. At 5.4 million barrels a day, US oil production had little impact on global supply.

You can see on the chart how esport levels for the two biggest oil producers — Russia and Saudi Arabia — spiked between 2000 and 2005. This spike in production correlates to the emergence of the Chinese economy.

China’s demand for oil spiked and so did prices. It was all Russia and Saudi Arabia could do to keep up.

Now, between 2005 and 2010, you can see where Russian and especially Saudi oil exports fell. This drop in exports correlates to the Great Financial Crisis.

This was also the era when the idea of Peak Oil really gained traction. As a theory, Peak Oil said that the world had discovered all the cheap, easy access oil. Peak Oil meant that all future discovery would come at a higher cost, like deep sea.

And so oil prices averaged $94 a barrel in 2008, and then fell to an average of $60 in 2009. Notice that even during the depths of the GFC, oil prices remained well above 2005 levels.

You’ll notice, too, that through all this, US oil production was still a non factor. The U.S. averaged just 4.9 million barrels a day in 2008, and 5.3 million barrels a day in 2009.

But that was about to change.

Higher oil prices due China’s spike in demand as it emerged as an economic powerhouse incentivized exploration and innovation in U.S. shale oil fields like the Bakken and the Permian Basin. And the Peak Oil thesis provided the talking points – that oil prices would remain high, thereby supporting the investment in shale.

So, companies didn’t start investing in fracking technology out of some sense of patriotic duty. Those early frackers like Continental and Hess and Kodiak and Brigham saw a market opportunity to make some money.

And making money will continue to drive US oil companies’ decisions about exploration and production.

The Oil Bear Market

In 2014, U.S. oil companies got a very good lesson about “drill, baby, drill,” from Saudi Arabia. Oil prices averaged over $100 a barrel in 2011, 2012 and 2013. Saudi Arabia didn’t like the fact that its exports to the U.S. fell so the Saudis decided to boost their own production as high as they could, crush oil prices and drive U.S. oil companies out of business.

On one hand it worked. Saudi opened the spigots and oil prices fell from over $100 into the $30s. Over 100 U.S. oil companies went bankrupt.

But on the other hand – the hand that the Saud’s thought they could grasp oil dominance with – it was a disaster. One, Saudi Arabia’s economy is completely dependent on oil revenue. And it needs oil to be at least $70-$80 to to balance the budget. So when oil prices fell onto the $30s it spent a big chunk of its foreign reserves – at least $250 billion – to plug the hole. Totally unsustainable.

Two, in 2015, the U.S. made it legal for U.S. oil to be exported again. Which meant that U.S. oil companies could compete with Saudi oil directly on the global stage.

And three, the Saudi “drill, baby, drill” plan was driven by a fundamental assumption: U.S. oil companies would not be able to adapt to lower oil prices. Sure, as I said, there were some bankruptcies. But there was also innovation. From the cost of fracking sand, to increased automation, to drilling rig costs – the entire cost structure of the U.S. oil business fell from around $55 a barrel to $35 a barrel, and sometimes lower than that.

Put another way, Saudi Arabia didn’t understand a fundamental function of capitalism – that competition drives innovation to lower costs.

Before the Oil Bear Market, the U.S. oil patch was free-wheeling. Taking on debt to “drill, baby, drill” was applauded. Stock prices soared.

Post-Oil Bear Market, oil companies are focused on balancing increased production with the investment and debt it takes to do it…

Managing the Flow

It’s all about managing the flow, as the recent oil mega-deals show.

On October 11, Exxon bought out Permian oil producer Pioneer for $56 billion. Two weeks later Chevron took out Hess for $52 billion.

The important thing about these deals is they don’t increase new oil production. Of course Exxon and Chevron could both invest billions to bring new oil to market. But what would that do to prices?

It’s a much better plan to pay a little premium to take over another company’s production and then manage flow to grow profits. Especially in Exxon’s case, the Permian oil and nat gas it got from the Pioneer acquisition is strategic. As I wrote on October 23:

Exxon has its Eagle Pass LNG terminal coming online for global export next year. The terminal sits on the Texas-Louisiana border, so having feedstock as close as the Permian Basin in Western Texas is an obvious benefit.

The bottom line is that “drill, baby, drill” is a fantasy. U.S. oil companies are all about managing the flow.

That’s it for me today. I’m traveling to Baltimore and Richmond on Wednesday for Thanksgiving with friends and family, so this is likely it for me this week. So take care, have a great and safe holiday and I’ll talk to you soon.

Briton Ryle

Chief Investment Strategist

Pro Trader Today

brit.ryle@protradertoday.com

Facebook: https://www.facebook.com/ProTraderToday

Twitter: https://twitter.com/BritonRyle